Keep these financial considerations in mind as you set a savings goal for your child’s education.

Even if your child’s college years are far off, the prospect of planning for education expenses can feel overwhelming.

College costs are significant, and they continue to outpace inflation. But those who start financial planning for their child’s education early often are more prepared when the time comes.

We can help you develop a personalized financial plan that can help you reach this goal, while also balancing it with other financial priorities.

As you begin the financial planning process for your child’s college education, here are a few things to think about.

- Understand the value and cost of a college education

- Consider your goals and priorities, especially retirement

- Keep in mind: The earlier you start, the better

- Estimate your savings goal

- Incorporate your savings goal into your financial strategy

- Questions to discuss with us

1. Understand the value and cost of a college education

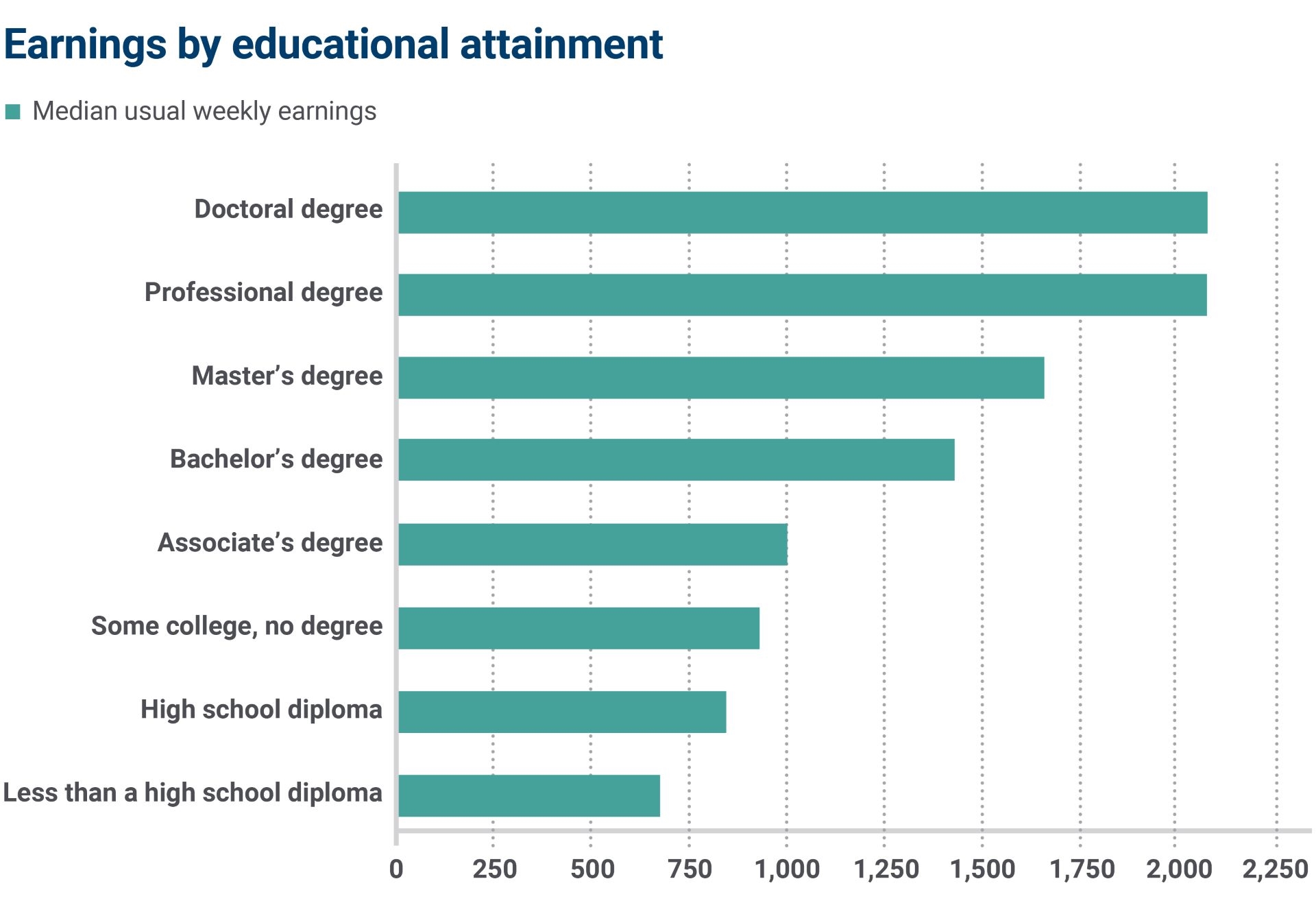

Though the cost of higher education keeps rising, it continues to offer a significant return on investment. The earnings from college graduates today on average far outpace those without a college degree, according to the U.S. Bureau of Labor Statistics.1

Note: Data are for persons age 25 and older. Earnings are for full-time wage and salary workers. Source: U.S. Bureau of Labor Statistics 2022, Current Population Survey.

The “real” cost of college

The average cost of college has increased significantly over the past several decades, with expenses generally growing faster than the rate of inflation.2

| | Public, four-year university,

in-state | Public four-year university, out-of-state | Private nonprofit, four-year college or university |

| Published charges for tuition, fees, room and board,

2023-2024 | $24,030 | $41,920 | $56,190 |

Source: College Board, Trends in College Pricing 2023, costs based on full-time enrollment.

There are also expenses beyond tuition and room and board to consider when financial planning for your child’s education. This includes books, technology and transportation. Even counting all that, the actual cost of attendance isn't always obvious because many families don't pay the advertised price. Luckily, schools are now required to have a net price calculator on their websites where you can get a breakdown of the real cost of attendance.

2. Consider your goals and priorities, especially retirement

What’s the most common way to pay for college? The largest single source of college funding for most American families still comes from parents’ income and savings, followed by scholarships and grants and borrowing, according to a 2021 survey conducted by student loan provider Sallie Mae.3

Consider your expectations for your child when it comes to helping cover the cost of college. How might you expect them to contribute? After all, there will be other financial goals, like your retirement, that take precedent over saving for education.

Learn more: How to save for retirement and college at the same time

3. Keep in mind: The earlier you start, the better

Education savings accounts, such as a 529 plan, can go a long way toward helping reach your financial planning goals, but the money you contribute needs time to grow.

By starting to financially plan for college early, you’ll not only give yourself and your child more options when it comes to financing their education, you’ll also give yourself options when it comes to your other financial priorities.

4. Estimate your savings goal

No parent can know for sure if their child will attend a private or public school, what they’ll study, or if they’ll earn a scholarship. At this point, you can make an educated guess about a savings goal — then prepare to adjust as a child’s goals may change down the road.

Use our college savings calculator

Get a sense of what your child’s higher education expenses may be and how much you may need to start saving to get there.

Review calculator

Potential gifts from families

As you think about your expected contribution to your child’s education, it’s also smart to think about other familial contributions. For example, have your child’s grandparents expressed interest in helping to finance a part of their education? If so, consider tax strategies to use this contribution most effectively.

Learn more: Tax strategies for college savings and gifting

5. Incorporate your savings goal into your financial strategy

Once you arrive at an amount to save for your education goal, you can determine the investment and savings vehicles you’ll use as part of your financial strategy.

Additionally, it’s not premature to think about what role, if any, financial aid and student loans will have in funding your child’s higher education. You won’t need to decide on this until the year before your child goes to school but having a general understanding of how the process works can help inform your journey.

Let’s create a financial strategy for your student’s education

With time, planning and our help, you can gain a better understanding of how much you’ll need for future education costs and create a financial strategy to help reach those goals.