Make the tax advantages of an HSA work for you now and in retirement.

Many Americans are familiar with how health savings accounts (HSAs) can help pay for current health care expenses. But, due to their tax benefits, HSAs can also be uniquely powerful retirement savings tools.

We can help you consider how to incorporate an HSA as part of your retirement strategy.

Whether you’re contemplating opening an HSA or already have one, here’s what to know about how these savings vehicles can benefit you today — and years from now.

In this article:

How HSAs work

An HSA is a tax-advantaged account that allows you to set aside pre-tax funds to pay for qualified medical expenses, with the option of investing the contributions to earn returns over time. To qualify for an HSA, you must be enrolled in a high-deductible health plan (HDHP).

Qualified medical expenses include but are not limited to:

- Coinsurance

- Copayments

- Deductibles

- Eyeglasses

- Dental services

- Medication

HSA contribution limits

|

2024 |

2025 |

| Individual |

$4,150 |

$4,300 |

| Family |

$8,300 |

$8,550 |

| Age 55+ catch-up contribution |

$1,000 |

$1,000 |

If you receive your health insurance through your employer, you can often make HSA contributions through a payroll deduction. Contribution limits apply to the total amount funded by you and your employer.

Learn more: Managing health care costs

HSA tax benefits

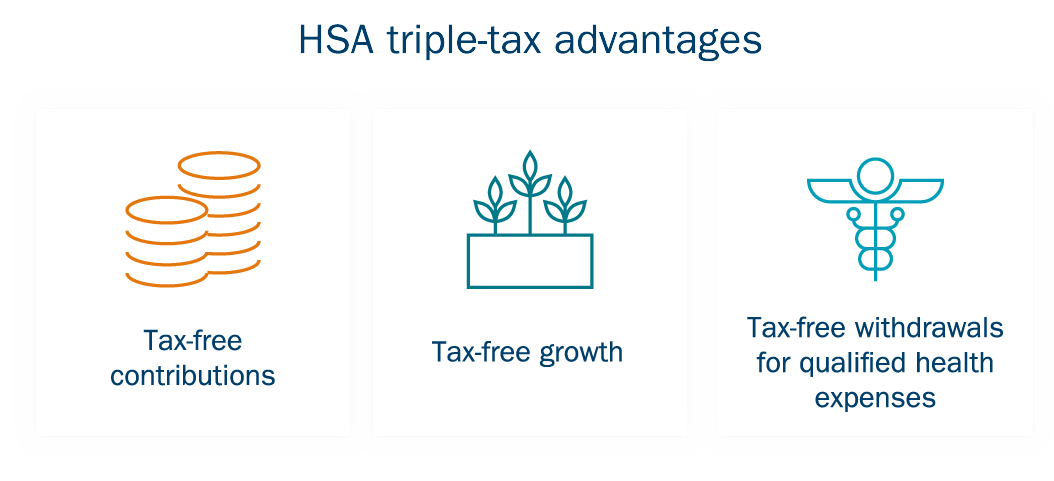

While HSAs can help offset the out-of-pocket costs associated with a high-deductible health plan, they are also uniquely powerful retirement planning tools, thanks to their triple tax advantages:

- Tax-free contributions: Contributions to your HSA are fully deductible from your federal income taxes, even if you don’t itemize. That gives you more money for qualified medical expenses, whether you pay for them now — or decades in the future.

- Tax-free growth: HSAs offer you the option to invest your contributions, and any growth in interest or earnings also isn’t taxed. Depending on how much you contribute and how long you allow your HSA to grow, your contributions and earnings can significantly compound over time. Also, unlike a 401(k) or an IRA, there are no required minimum distributions (RMDs). The HSA account has the potential for growth over time, even if you do not open an HSA until later in life.

- Tax-free withdrawals: Provided it is for qualified health expenses, any money you withdraw from your HSA is tax-free.

Learn more: What to know about health insurance and taxes

HSAs vs. health care FSAs

It’s common to confuse HSAs with health care flexible spending accounts (FSAs), which have similar objectives but different benefits and limitations. Health care FSAs allow individuals to use tax-free dollars to pay for the same types of medical expenses as an HSA, however there are a few key differences:

|

|

HSA

|

FSA

|

|

Eligibility

|

Must be enrolled in a high-deductible health plan (HDHP) to qualify. Does not need to be part of an employer-sponsored group plan.

|

Must be part of an employer-sponsored group health plan.

|

|

Contribution

limits

|

$4,300 for an individual and $8,550 for family coverage in 2025. Those 55 and older can make an additional $1,000 catch-up contribution.

|

$3,300 in 2025.

|

|

Ownership and portability

|

You own your HSA and can keep the account if you leave your current employer.

|

Owned by the employer and is not portable.

|

|

Tax benefits

|

Triple tax benefits: tax-free contributions; tax-free investment growth; and tax-free withdrawals for eligible medical expenses.

|

Tax-free contributions; withdrawals are tax free for eligible medical expenses.

|

|

Option to invest?

|

Offers the option to invest contributions.

|

Does not offer the option to invest contributions.

|

|

Rollover?

|

Unused balance rolls over into the next year.

|

Use it or lose it; unused funds are forfeited unless the employer allows rollovers (which are capped at $640).

|

Check with your employer for details on their rules around FSAs and rollovers.

HSA limitations

While HSAs offer significant tax benefits, there are a few considerations investors should be aware of:

- There is a tax penalty if used improperly: If you use your HSA to pay for nonqualified expenses, you will have to pay income tax on the nonqualified distributions. Additionally, if you’re under the age of 65, you will also be subject to a 20% penalty.

- You cannot deduct medical expenses paid for by an HSA: When filing your taxes, medical expenses that were paid with HSA funds cannot be deducted. This would be considered “double dipping” as HSA funds are already exempt from taxes.

Invest your HSA for the long-term

Because of their long-term growth potential and tax benefits, HSAs can be especially beneficial if you are already maxing out contributions to a 401(k) or an IRA. For these investors, an HSA can effectively function as a tax-advantaged retirement fund earmarked for health-care expenses.

However, to take full advantage of all the tax benefits, you will need to take the extra step to invest the money in your HSA. It’s a common mistake for investors to set aside money in their HSA, but then not invest the money. Make sure you’re taking advantage of the tax-free growth that an HSA affords.

Ways to leverage your HSA for retirement

Health care is often one of the most significant expenses people face in retirement. The tax benefits of an HSA offer a powerful way to help pay for those expenses, especially if the funds in your account have a long time horizon. Here are a few HSA considerations for retirees:

- Pay for health care and medication needs: Once you enroll in Medicare, you can no longer contribute to an HSA. However, you can use HSA funds to pay for many Medicare expenses, including premiums for Part B, Part D and Medicare Advantage plans (though you cannot use an HSA to pay for Medigap premiums). If you continue to work past 65 and have an employer-sponsored health plan, you can also use your HSA to pay for those premiums.

- Cover long-term care expenses: HSAs can be used to pay for in-home nursing care, nursing home fees and long-term-care expenses, including premiums for long-term care insurance, provided the policies are “tax-qualified.”

- Pay for non-medical expenses penalty-fee: Once you turn 65, you can use your HSA to pay for non-medical expenses without incurring the tax penalty typically levied for nonqualified HSA distributions. However, any HSA funds used this way will be taxed as income.

- Bridge the gap to Medicare: If you retire or stop working before becoming eligible for Medicare, you will still need health care. If you don’t have access to adequate coverage through your spouse or the marketplace, one option is COBRA, which allows you to continue coverage under your old employer-sponsored plan for up to 18 months. While COBRA can be expensive, it offers a significant benefit if you have an HSA. Though insurance premiums are not generally considered qualified medical expenses for an HSA, you can pay for your COBRA premiums with HSA funds. However, once you turn 65, you will need to sign up for Medicare, as having COBRA coverage does not qualify you to delay signing up without incurring a late-enrollment penalty.

Work with us today to meet tomorrow’s financial goals

We can help you determine how this tax-advantaged account can help you meet your short-term and long-term goals.